Methodologies for Defining Objectives: A Strategic Approach

Updated: 2026-07-07

A poorly defined objective is no better than having none. "Improve sales", "be more agile", or "increase customer satisfaction" are intentions, not objectives. The difference between an intention and a useful objective is that the objective includes an unambiguous success criterion and a deadline. The SMART, OKR, and Balanced Scorecard methodologies have been articulating that difference for decades. This article explores how they work, when to use each, and what implementation failures make them fall apart.

Key takeaways

-

Strategic objectives must be specific, measurable, and time-bound: all three methodologies share this core.

-

SMART is a validation criterion for individual objectives; OKR is a vertical alignment system for the organisation; Balanced Scorecard is a comprehensive strategic management framework.

-

The choice of framework depends on organisation size, management team maturity, and existing measurement culture.

-

The most frequent mistake is adopting the methodology’s vocabulary without changing the underlying decision process.

-

Without a periodic review system (weekly, monthly, quarterly), any objective methodology dies from disuse.

Why most objectives fail

Research on organisational performance management points to three recurring causes of failure:

-

Ambiguity: the objective doesn’t define what counts as success. "Improve customer satisfaction" can mean anything until a KPI and threshold are specified.

-

Vertical disconnection: team objectives don’t derive from organisational objectives, or vice versa. Each area optimises its small domain without clear contribution to the whole.

-

No review: objectives are set in January and not reviewed until December. By then, context has changed and objectives are irrelevant or achieved without effort.

All three methodologies address these three problems in different ways.

SMART: the baseline validation criterion

SMART is an acronym defining the attributes a well-formed objective must have. George Doran proposed it in 1981, and although his original version used "assignable" and "realistic", this is the variant used almost everywhere today (Wikipedia[1]):

-

Specific: the objective describes a concrete action or result, not a general direction.

-

Measurable: a quantitative indicator exists to determine whether the objective has been met.

-

Achievable: the objective is challenging but realistic given available resources.

-

Relevant: the objective contributes to the organisation’s strategy.

-

Time-bound: there is a review or closing date.

SMART is not a management methodology: it is a quality filter. An objective that doesn’t pass the SMART filter shouldn’t be accepted. Its limitation is that it says nothing about how objectives relate to each other or to overall strategy — for that, OKR or Balanced Scorecard is needed.

OKR: vertical alignment and ambition

OKR (Objectives and Key Results) was introduced by Andy Grove at Intel in 1971 and later adopted massively by Google, Spotify, LinkedIn, and dozens of technology companies. This article treats it as one piece of the puzzle alongside SMART and Balanced Scorecard; for a full treatment of the method see OKR methodology. Its structure is:

-

Objective: an ambitious qualitative statement that answers "where do we want to go?" It has no number, but has clear direction.

-

Key Results: 2-5 quantitative metrics that answer "how do we know we’ve arrived?" These are the measurable indicators that define objective success.

Example:

- Objective: become the benchmark reference in our vertical market.

- KR1: increase NPS from 38 to 55 before Q3.

- KR2: secure 3 published success cases with enterprise clients of over 500 employees.

- KR3: reach 25% share in the mid-market segment per the Gartner sector report.

The power of OKR lies in the cascade: company OKRs break down into area and team OKRs, creating vertical alignment. A developer on the product team can see how their KR of "reduce page load time to < 2s" contributes to the company KR of "improve conversion rate by 15 points".

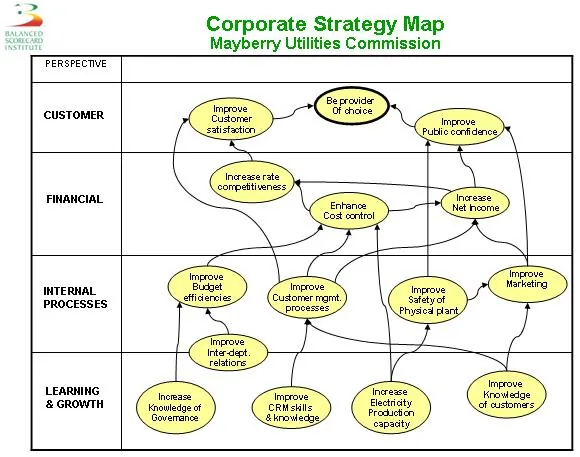

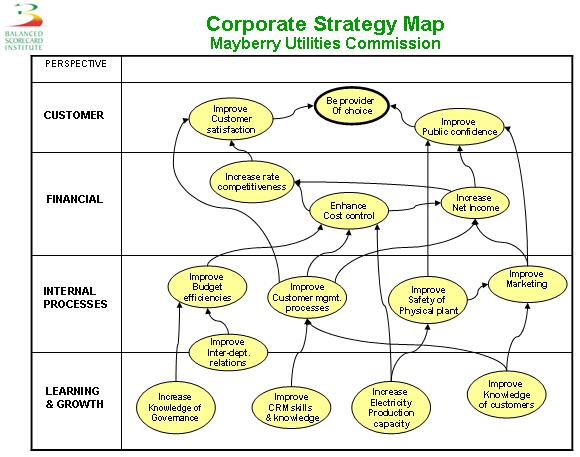

Strategy map relating the four Balanced Scorecard perspectives: financial, customer, internal processes, and learning

Strategy map relating the four Balanced Scorecard perspectives: financial, customer, internal processes, and learning

OKRs are typically quarterly and set a success threshold of around 70%: if 100% of all KRs is consistently achieved, the objectives weren’t ambitious enough. Google, which documents its own use of the method, places the "sweet spot" between 60% and 70% (Google re:Work[2]). This differentiates OKRs from operational KPIs, where 100% is indeed what’s expected; that same measurement rigour is what startup metrics demand.

Balanced Scorecard: strategy across four perspectives

The Balanced Scorecard (BSC), which Kaplan and Norton introduced in Harvard Business Review in 1992 (HBR[3]), proposes that an organisation’s strategy translates into objectives and indicators across four complementary perspectives:

-

Financial: what financial results must the strategy produce? (revenue, margins, EBITDA, ROI).

-

Customer: what value proposition does it offer customers? (satisfaction, retention, market share, NPS).

-

Internal processes: what processes must it improve to deliver that value proposition? (cycle time, quality, innovation).

-

Learning and growth: what organisational capabilities does it need? (team competencies, culture, technology).

The BSC’s central hypothesis is that financial indicators are lagging indicators: they measure past results. The customer, process, and learning perspectives contain leading indicators that predict future financial results. Managing only the financial ones is managing by looking in the rear-view mirror.

BSC is especially useful in large organisations with multiple business units, where strategic coordination is the main challenge. Its limitation is implementation complexity: developing a coherent strategy map and keeping it updated requires a structured process and executive commitment.

How to implement without failing

Objective methodologies almost always fail for the same reasons:

-

Adopting the vocabulary without changing the process: calling what were previously "annual targets" "OKRs" changes nothing. The difference lies in ambition (70% as success), review frequency (quarterly), and transparency (OKRs public across the organisation).

-

Too many objectives: OKR recommends 3-5 objectives per level with 2-5 KRs each. More than this generates dispersion.

-

No periodic review: weekly or biweekly check-ins are part of the system, not an additional burden. Without review, OKRs are decoration.

-

Linking OKRs to variable compensation: when a bonus depends on KRs, people negotiate them down to guarantee payment. OKR and performance evaluation are separate systems.

Implementing any objective framework requires the same discipline recommended in recommendation systems: evaluate with the right metrics and at the right frequency. An objective without periodic review is an artefact, not a management tool.

Conclusion

SMART, OKR, and Balanced Scorecard frameworks are not bureaucracy: they are systems for turning strategy into measurable, aligned commitments. SMART validates that each objective is well-formed; OKR vertically aligns organisational ambition; Balanced Scorecard connects financial indicators with their causes in processes and people. Choosing the right framework and maintaining the discipline of periodic review is what separates organisations that execute their strategy from those that reformulate it every year.

This article is also available in Spanish.