The Spanish draft law transposing NIS2 is still in parliament in 2026, but the directive's technical obligations have applied since October 2024. Practical map: the ten minimum security measures, the 24-hour, 72-hour and one-month incident notification window, and the new supply-chain security obligations.

Capital concentration in frontier labs makes the first round harder for founders without a Silicon Valley network, but alternatives have multiplied: revenue-based financing for recurring ARR, improved venture debt after the SVB collapse, public grants like ENISA and CDTI Neotec, and AI-leveraged bootstrapping that shrinks the team you need.

While OpenAI and Anthropic dominate headlines with rounds worth hundreds of millions, a growing group of niche AI startups generates one to ten million dollars in revenue with teams of two to ten people. They share five patterns: narrow vertical focus, 70-80% margins, community distribution, iteration cycles in days, and AI as an internal lever.

Product-market fit for LLM-powered products still depends on the same classic signals: cohort retention, NPS, and revenue expansion. What changes are the higher quality baseline, faster competitor iteration, and where durable moats come from: proprietary data, workflow integration, and network effects.

Industrial as-a-service flips equipment sales into outcome sales: Rolls-Royce charges per flight hour, Philips per lux delivered, and several manufacturers guarantee uptime through maintenance contracts. It works when real telemetry, clear SLAs, solid financing, and aligned incentives are all in place; without those four, it stays marketing and the vendor never actually assumes risk.

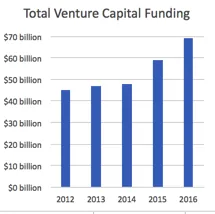

The venture capital market in 2024 has partially recovered, but the improvement is uneven. Generative AI absorbs 35-40% of capital while consumer and DTC remain slow. Due diligence timelines have tripled, the burn multiple now dominates investor conversations, and a serious raise takes three to six months from first pitch to close.

The SaaS market is consolidating after years of fragmentation: private equity acquisitions, licence changes, and double-digit price hikes have shifted negotiating power toward vendors. A practical framework to audit your exposure, build credible migration pressure, and design exit strategies that work when you actually need them.

5 min1964.6

We use first- and third-party cookies to analyze site traffic. You can accept them, reject them, or configure your choice.

Learn more about cookies

Cookie preferences

NecessaryEssential for the site to work. Always on.

AnalyticsHelp us understand how the site is used (Google Analytics).